Saving money on a low salary can feel like an uphill battle. When most of your paycheck goes toward rent, groceries, transportation, and utility bills, it may seem like there is nothing left to save. For many people, the idea of building savings feels unrealistic when basic expenses already consume a large portion of their income.

However, saving money is not only about how much you earn. It is largely about how you manage the money you already have. With the right systems, habits, and mindset, it is possible to build savings even on a modest income. The key is learning how to reduce unnecessary spending while still enjoying the parts of life that matter to you.

You do not need to give up everything you enjoy or live an extremely restrictive lifestyle to grow your savings. By making smarter financial choices and focusing on high-impact strategies, you can start saving money faster than you might expect.

1. The “Low Salary” Reality Check

Many financial experts recommend the 50/30/20 budgeting rule, where 50% of income goes toward necessities, 30% toward personal spending, and 20% toward savings. While this rule can be helpful as a general guideline, it does not always reflect the reality of people living in expensive cities or working with limited income.

For example, rent alone might consume half—or even more—of your monthly earnings. When that happens, the traditional budgeting rule can feel discouraging and unrealistic.

The Fix: The Percentage-First Method

Instead of trying to force your finances into a strict rule, start with a much simpler strategy: save a small percentage of your income first.

For example:

- If you earn $2,000 per month, start by saving 1%, which is just $20.

- Set up an automatic transfer that moves this money into a savings account as soon as your paycheck arrives.

- Every three months, increase the percentage slightly.

This method helps you build the habit of saving without dramatically affecting your daily lifestyle. Over time, even small increases can create meaningful progress.

The goal is not perfection. The goal is consistency.

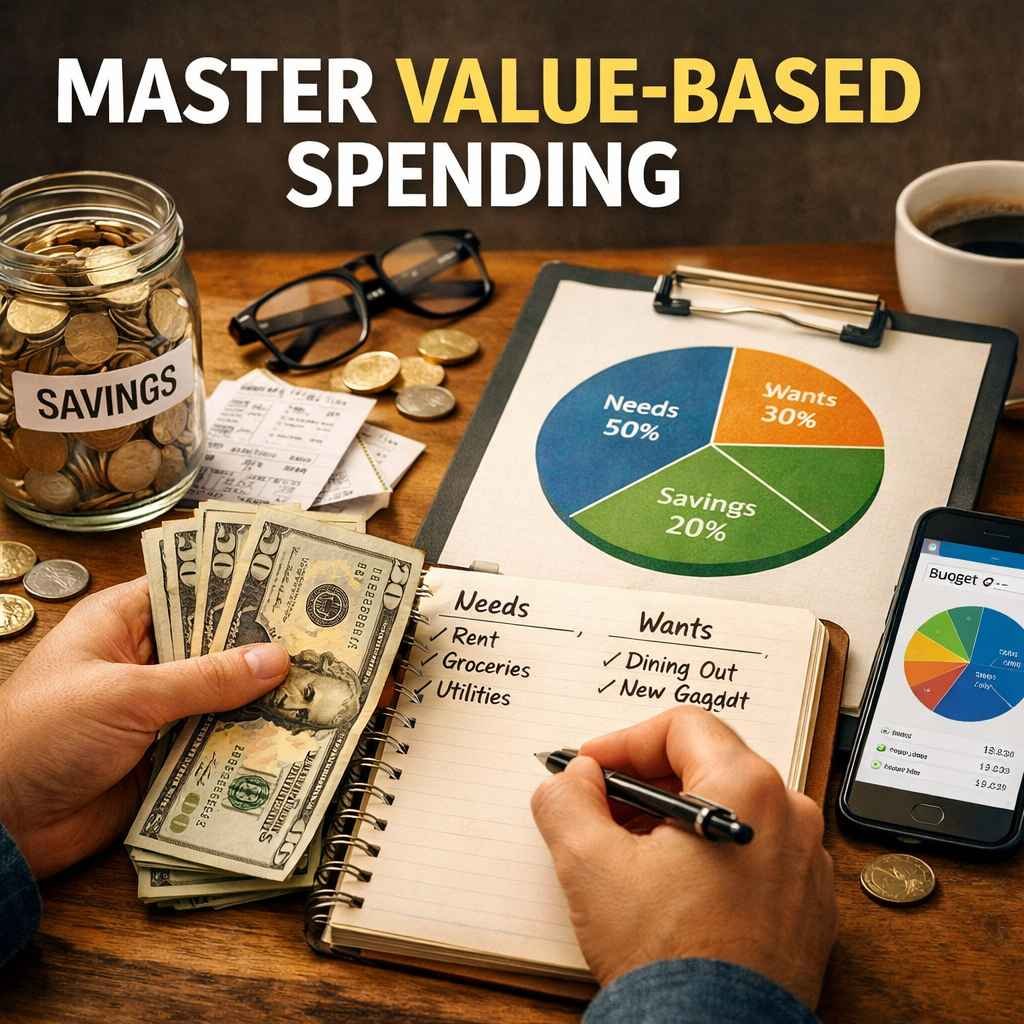

2. Master Value-Based Spending

One of the biggest mistakes people make when trying to save money is cutting everything at once. This approach often leads to frustration and eventually causes people to abandon their financial goals.

A better approach is value-based spending.

Instead of eliminating all non-essential spending, focus on the few things that truly make you happy.

Identify Your “Big Three”

Ask yourself a simple question:

What are the three non-essential things that genuinely improve my quality of life?

Your list might include things like:

- A weekly takeout meal

- A gym membership

- Your favorite streaming service

- Morning coffee from your favorite café

Keep these things in your budget. They add value to your life and help you maintain a lifestyle you enjoy.

Then reduce spending on everything else that does not bring the same level of satisfaction. This approach removes the feeling of deprivation because you are intentionally protecting the experiences you care about most.

3. Substitution, Not Elimination

A powerful way to save money quickly is through substitution instead of elimination. This means replacing expensive habits with more affordable alternatives rather than completely giving them up.

Here are a few examples:

| Instead of… | Try… | Estimated Monthly Savings |

| $12 daily work lunch | Sunday “big batch” meal prep | $200+ |

| Multiple streaming subscriptions | Rotate one service each month | $40–$100 |

| Frequent restaurant takeout | Homemade “Fakeaway” meals | $100+ |

| Impulse online shopping | 48-hour wishlist rule | $50–$150 |

Pro Tip: The “Fakeaway”

If you enjoy ordering takeout regularly, try learning how to cook one or two of your favorite dishes at home. This concept is often called “Fakeaway”, meaning homemade versions of restaurant meals.

For example, if you love Thai food, learning to make a simple Pad Thai at home might cost around $5 per meal instead of $20 for delivery. Over time, this small change can save hundreds of dollars while still allowing you to enjoy the foods you love.

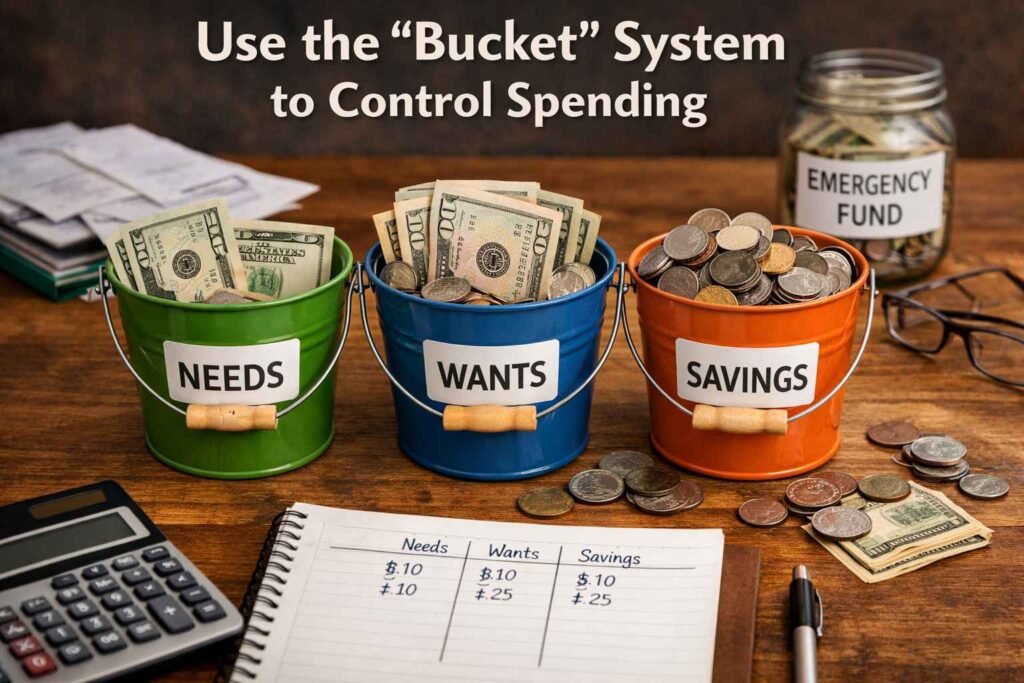

4. Use the “Bucket” System to Control Spending

Modern digital payments make spending extremely easy. When you pay with a card or smartphone, it can feel like the money is not really leaving your account.

This “frictionless spending” is one of the biggest reasons people struggle to save money.

A helpful solution is the Bucket System, sometimes called the envelope method.

Digital Buckets

Many banking apps allow you to create multiple savings categories, often called vaults, buckets, or spaces. You can divide your income into separate sections such as:

- Rent

- Groceries

- Transportation

- Emergency savings

- Entertainment

By assigning money to each category, you gain a clearer picture of how much you can safely spend.

The “Cash for Fun” Rule

Another effective strategy is to use physical cash for discretionary spending.

For example, you might withdraw $40 or $50 in cash for the week to cover entertainment, snacks, or small purchases. When the cash runs out, the spending stops until the next week.

This method creates a clear boundary that is much harder to ignore than a digital payment.

5. Quick Wins That Free Up Money Immediately

If you want to save money quickly, start by identifying hidden expenses that may be draining your income.

The Subscription Audit

Many people pay for services they no longer use. Streaming platforms, mobile apps, and subscription boxes can quietly accumulate over time.

Take a few minutes to review your bank statement and cancel any services you rarely use. Even a $7 monthly subscription adds up to $84 per year.

The Insurance Negotiation

Another easy strategy is to call your car or renter’s insurance provider and ask if there are any available discounts.

You might say something simple like:

“I’ve been reviewing my expenses. Are there any loyalty discounts or adjustments that could lower my monthly premium?”

In many cases, companies are willing to offer discounts to keep long-term customers.

Small Utility Adjustments

Small changes to your energy usage can also lower your monthly bills. For example:

- Lower your thermostat slightly during winter.

- Raise it slightly during summer.

- Turn off electronics when not in use.

These adjustments may seem small, but they can reduce energy costs by several percent each month.

6. The 24-Hour (or 48-Hour) Rule

Impulse purchases are one of the biggest obstacles to saving money on a tight budget.

A simple solution is the 24-hour rule.

When you see something you want to buy online, add it to your shopping cart but wait at least one full day before completing the purchase.

Often, the excitement of discovering the item creates a temporary rush of dopamine. By the next day, the urge to buy it may disappear.

If you still genuinely want the item after waiting, then you can reconsider the purchase.

This small habit can prevent many unnecessary expenses.

The Bottom Line

Saving money on a low salary is not about extreme sacrifice. It is about intentional spending and smarter financial habits.

When you focus your money on the things that truly matter and eliminate the expenses that do not add value to your life, saving becomes much easier. Small strategies like automation, substitution, budgeting buckets, and impulse control can create meaningful progress over time.

Even saving a small percentage consistently can build financial confidence and stability.

Start today by moving just 1% of your income into a savings account. It may seem like a small step, but it creates momentum—and momentum is what ultimately leads to lasting financial success.

Leave a Reply